Why conduct a corporate carbon footprint? What is it for?

This question, many companies ask themselves.

For the record, a carbon footprint is a snapshot at a given moment of all greenhouse gas emissions from a company.

Measuring is good but it is not enough. It is in fact the starting point of a strategy to reduce GHG emissions: we only reduce what we know. This reduction strategy is materialized by an action plan. The latter is in fact mandatory in the realization of a Bilan Carbone® or in the Diag Decarbon’Action device.

Reducing emissions, beyond the obvious climate interest, is also a lever for better economic performance.

Why? Because reducing emissions often allows you to save money at the same time. This is what we learn from the work of our Expertise team.

Measuring and reducing emissions also allows you to protect yourself from the increase in the price of carbon, transition risks and competitive risks.

In short, investing in a carbon footprint is investing in an essential tool of a global strategy and not just in the company's climate or CSR strategy.

1. The economic performance of an action plan

1.1 Mostly profitable actions

The Sami expertise team has been working for several months on the economic assessment of action plans that can be implemented within companies to reduce their emissions.

For nearly 60 actions, which concern mobility, logistics, energy, eco-design or even digital technology, our experts have carried out, for each of these actions, a financial evaluation and a carbon evaluation.

In short, from a financial point of view, it is a question of calculating the sum of the financial costs with and without the implementation of the action. And from a carbon point of view, to calculate the emissions with and without the implementation of the action.

These two evaluations make it possible to calculate what is called the cost per tonne of CO2 avoided: for one tonne of CO2 avoided, how much will it cost net, i.e. by subtracting from the investments the savings linked to the operational costs of the action. If this cost is negative, it means that the action is financially profitable (possibly after a certain number of years), otherwise it means that it will cost the company more to deploy this action.

Result, out of the 57 actions evaluated, 48 are profitable over the life of the action.

Some examples:

"We realize that for many of the actions implemented, there is an alignment between carbon interest and financial interest. The company has a financial interest in implementing these actions because they are profitable. And they will at the same time allow to reduce greenhouse gas emissions."

Guillaume Colin, Head of expertise, Sami.

1.2 How are these results obtained?

In order to carry out the financial and carbon evaluations, two indicators are used: the CAPEX which translates the investment costs necessary for the implementation of the action and the OPEX which translates the operational or variable costs linked to the implementation of the action. The latter are very often negative because the actions implemented allow to save energy consumption and therefore money every year over the entire life of the action.

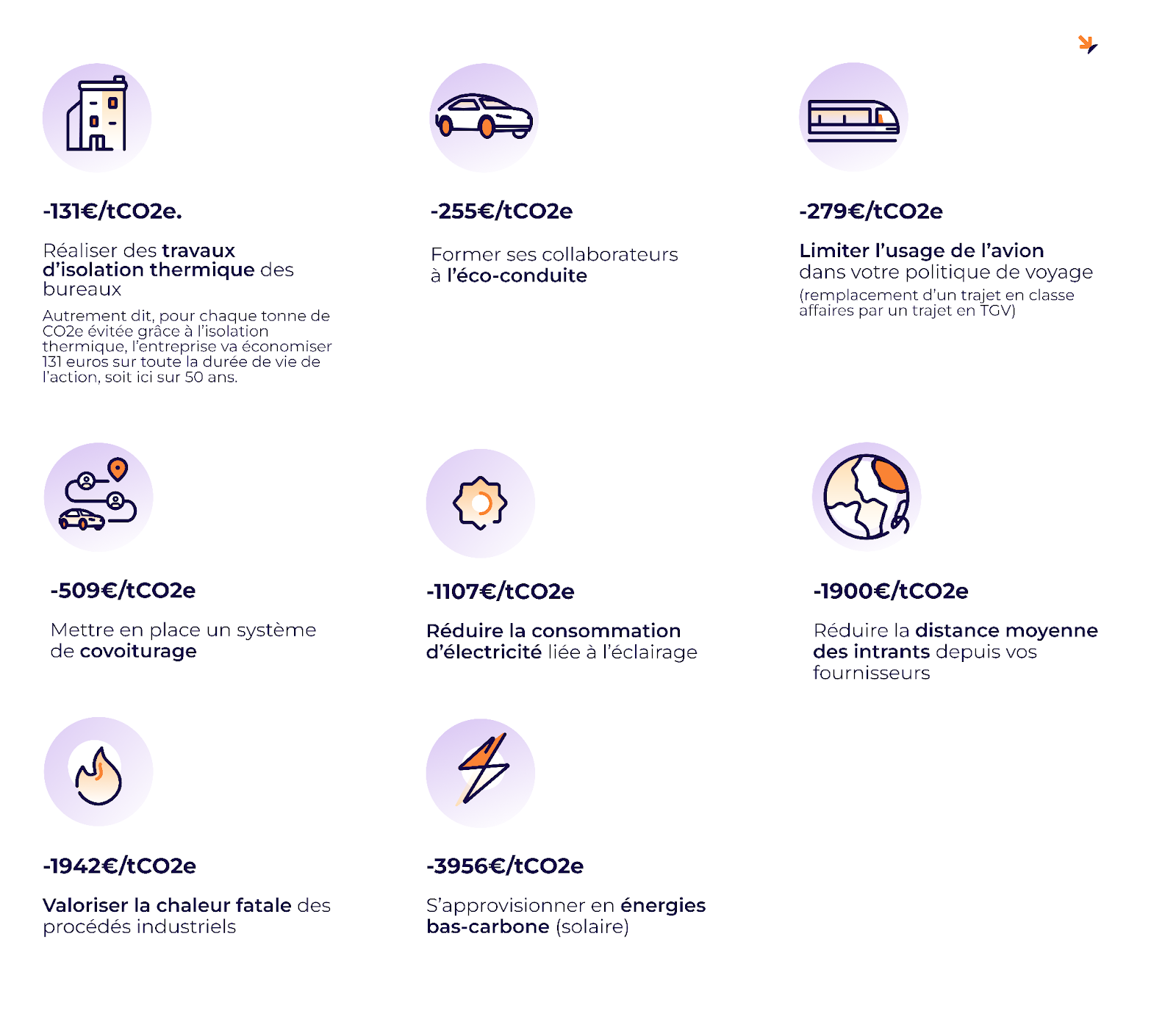

Take the example of the thermal renovation of offices.

- Financial CAPEX: this is the average amount of thermal renovation work (from 200 to 400€ per m² of renovated surface).

- Carbon CAPEX: these are the initial emissions emitted during the thermal renovation work (approximately 190 kgCO2eq per m² renovated according to the OID).

- Financial OPEX: this is the difference between the amount of the energy bill after the energy renovation work and this same bill before the renovation work (we go from approximately 12 € of operating costs per m² before renovation, to approximately 2 € per m² after renovation).

- Carbon OPEX: this is the difference between the emissions related to the heating of the premises after the renovation and these same emissions before the work (we go from approximately 55 kgCO2eq per m² before renovation, to approximately 10 kgCO2eq per m² after work).

Over 50 years, the lifespan of a thermal renovation, this action thus saves 131 euros for each tonne of CO2 avoided.

1.3 Sobriety, efficiency and low-carbon energies, different profitability horizons

"Sobriety actions are those that are the most profitable because they do not require, or very little, investment costs - their indirect cost lies in the feasibility of behavioral or organizational changes." On the contrary, some efficiency actions and those of implementing low-carbon energies are more costly to invest in and therefore the payback time will be longer." Guillaume Colin.

Thus, limiting air travel in its travel policy is, for example, a sobriety action that is immediately profitable. This is also the case for lowering the heating by 1 degree in its premises (no investment cost but a reduction in emissions and immediate financial savings) or training its employees in eco-driving: the cost of the training is low compared to the financial savings and the reduction in emissions allowed by this action.

On the other hand, the profitability horizon is longer for most efficiency actions and those on the deployment of low-carbon energies and technologies. This is the case of our example of thermal renovation of buildings. The initial investment costs inevitably require waiting a few years before the work is financially profitable.

The maturity of the actions implemented is also an important factor of profitability since very often the most expensive actions concern technologies that are still little tested or little deployed on a large scale: e-fuels, hydrogen or even CO2 capture and sequestration.

1.4 The interests and the limits of the action plan's costing

Calculating the costs per tonne of CO2 avoided for each measure thus makes it possible to cost the overall cost of an action plan for a defined volume of emissions to be reduced. This element thus integrates the company's decarbonization strategy.

Beyond the overall cost, the cost per tonne of CO2 avoided can also allow the company to define a prioritization in the implementation of the action plan:

- in increasing order of cost per tonne of CO2, i.e. starting with negative costs therefore profitable actions.

- by payback time: implementing first the most profitable actions in the short term for example.

However, the cost per tonne of CO2 avoided and the economic costing of the action plan cannot and must not be the only criterion in the implementation of measures to reduce greenhouse gas emissions.

First of all because the cost per tonne of CO2 avoided is above all an estimate. It is not a question here of a calculation to the euro of the fact of the uncertainties around in particular the price of carbon or the price of energy in the years to come. Let's take our example of thermal renovation of buildings again. In order to calculate the operational or variable costs (OPEX), it is necessary to necessarily integrate an energy price and therefore to make assumptions about the future developments on the energy markets (will the prices remain stable, increase or decrease?).

The cost per tonne of CO2 must therefore be seen as an indicator making it possible to give orders of magnitude. It is also possible to distinguish several price scenarios (for example low price, median price or high price of energy) in order to refine the costing and the profitability results.

Another limit of the cost per tonne of CO2 avoided, it highlights the sobriety actions for which, as we have said, the investment costs are zero or low and therefore the actions which are immediately or almost immediately profitable. This is an obviously very interesting and necessary lever to achieve our climate objectives but some of these actions have a fairly low potential for reducing emissions compared to efficiency actions or the implementation of low-carbon energies, requiring more costly investments. These sobriety actions (reduction of heating temperature, carpooling for employees or limitation of air travel in professional travel for example) also call for behavioral changes and are therefore sometimes difficult to accept among employees. The action plan cannot therefore be limited to these actions only.

Finally, just because a measure has a positive cost per tonne of CO2 avoided does not mean that the company should do nothing. Because in many situations, the cost of inaction will actually be much higher, in the short or medium term, than the cost of action.

This is also the other major economic interest of the carbon footprint: being able to protect oneself from the physical and transition risks to come which are sometimes today hidden costs but which risk weighing more and more in the years to come.

2. The carbon footprint, or how to anticipate transition risks

Transition risks are the impacts (positive and negative) related to the implementation of a low-carbon economy.

2.1 Remain competitive

More and more companies want to decarbonize their purchases, inputs often being a very important source of emissions. Reducing their direct emissions will not be enough to achieve their climate objectives. They must therefore ensure that they can also reduce the emissions of their value chain and therefore those of their suppliers.

This is why large companies, for example, are increasingly attentive to the carbon footprint of their purchases.

15 major French groups (EDF, Engie, Sanofi, Orano, ADP, Bouygues Construction, Thalès, Naval Group, Schneider Electric, Crédit Agricole, Safran, Equans, MBDA, Société Générale and GRDF) have thus joined the Alliance for Decarbonization and Energy Transition launched by the association PactePME in order to support SMEs and ETI, which are their suppliers, in their decarbonization. Alliance in which Sami is the main operator for supporting suppliers.

We can also mention the French National Lottery which launched in December 2023 a program to reduce the carbon footprint of its suppliers, Schneider Electric which wants to push its 1000 largest suppliers to reduce their CO2 emissions by half by 2025 or the SNCF which has integrated since last year for its 55 largest suppliers a carbon tonne price in its tenders in order to monetize their GHG emissions.

And doing nothing about emissions related to the supply chain could cost companies up to 500 billion dollars a year by 2030 worldwide. This is the result of the report published by EcoVadis and Boston Consulting Group (BCG) in 2025. The emissions of scope 3 are on average 21 times higher than the emissions of scopes 1 and 2, according to the data analyzed in the report.

On the contrary, always according to this report, up to 50 % of the emissions of the suppliers can be reduced without net cost, with a return on investment estimated between x3 and x6.

Accelerating its decarbonization is therefore both a factor of competitiveness in the face of increasing demands from customers and a means of protecting itself against the major financial risk associated with scope 3 emissions.

Finally, this dimension is not reserved only for the private sector. The law on the green industry, published on October 23, 2023, endorses the mandatory implementation as of July 2024 of environmental criteria and in particular greenhouse gas emissions in public tenders.

2.2 Anticipate the rise in the price of carbon

The price of carbon is also a major factor for the competitiveness of companies.

As we said earlier, it is impossible to predict what its exact price will be in 2, 5, 10 or 20 years. That said, with the strengthening of regulations, there is a strong chance that this price will increase regularly and considerably in the long term in order to promote decarbonization.

On the European market, the Carbon Border Adjustment Mechanism (CBAM) came into force on January 1, 2026. Gradually, suppliers outside the European Union in highly polluting sectors (cement, aluminum, fertilizers, etc.) will be taxed based on the carbon intensity of their exports to the European market. In parallel, new sectors will be integrated into this European carbon market, free pollution rights will be gradually removed and emission quotas will be reduced.

All these elements should contribute to fueling in the coming years and decades a rise in the price of carbon. On the EU Emissions Trading System (EU ETS), the price of the quota is today around 60 euros per tonne of CO2 after reaching 100 euros in February 2022. But according to economists from the London Stock Exchange Group, the new climate objective of the European Union (a reduction in emissions of 90% by 2040) could push the price of carbon above 400 euros per tonne by 2040, more than 5 times higher than today. This price of 400 euros would thus represent, according to the authors, the “potential cost to which companies that fail to decarbonize by this horizon will be exposed”.

“If a company wants to know its exposure to this financial risk of carbon, the starting point is to know its emissions. If it does not know to what extent its value chain is carbon-intensive, it risks paying much more for its raw materials or being less competitive downstream because these carbon taxes will erode its margins."

Guillaume Colin

2.3 Meeting new regulations

In France, a greenhouse gas emissions assessment, the BEGES, is mandatory at least every 4 years for companies with more than 500 employees. This BEGES must include significant indirect emissions (scope 3) since January 1, 2023.

The largest companies will all have to implement the European directive on extra-financial reporting, the CSRD.

Among the new reporting standards, one is entirely devoted to climate change, the ESRS E1. Companies will thus have to report, each year, their complete greenhouse gas emissions (scopes 1, 2 and 3) but also present what their climate transition plan is, how this plan allows them to move towards an objective compatible with limiting global warming to 1.5 degrees, what actions are being implemented to achieve the objectives set by the company, what means are being deployed to achieve them or even what are the anticipated financial effects of the physical and transition risks related to climate.

Moreover, the carbon footprint is the gateway to measuring the company's impact on the climate but also the impact of the climate (via the financial transition risks it induces) on the company.

On December 16, 2025, the European Parliament voted to simplify the CSRD. The companies subject to this text are those that:

- have more than 1000 employees

- generate more than 450 million euros in turnover

And to meet the requirements of extra-financial reporting, these companies will demand carbon data from their suppliers.

3. Subsidies for a carbon assessment

Diag Decarbon'Action

Diag Decarbon'Action is a device to support companies in carrying out a carbon footprint. This offer is operated by Bpifrance, co-financed by the ADEME.

The Diag includes a carbon assessment, the co-construction of a climate strategy to reduce greenhouse gas emissions and support in implementing the first measures of the action plan.

Companies with fewer than 500 employees that have never carried out a carbon assessment before are eligible. After the subsidy, the price is 6000 euros for all companies.

To understand everything about Diag Decarbon’Action, its terms, the support offered to companies, we invite you to watch the replay of our workshop held in September 2023 with the BPI and dedicated to the financing of the carbon assessment.

{{newsletter-blog-3}}

Mission Décarbonation

Don't miss the latest climate news and stay ahead of regulatory changes

Carrying out a carbon assessment with Sami

Sami helps you measure your emissions and implement an action plan

.avif)

.avif)

Les commentaires