The term "carbon accounting" (carbon accounting) broadly refers to the methods used to integrate the issue of climate change into the CSR strategy and policies of companies. Carbon accounting is very often used to more precisely describe the set of methods used to count, quantify and classify the greenhouse gas (GHG) emissions of a company, a community, an association over a given perimeter.

Carbon accounting therefore allows a company to assess the greenhouse gas emissions generated by its activity and that of its value chain and therefore to assess its dependence on carbon.

However, it is possible to distinguish two types of carbon accounting: general carbon accounting and analytical carbon accounting.

The first, the general one, offers a general view of GHG emissions and can meet the regulatory requirements to which companies are subject. The second, the analytical one, makes it possible to go into the detail of the emissions, post by post, entity by entity, subsidiary by subsidiaries, in order to build behind a targeted and effective action plan.

1. Carbon accounting and financial accounting

We talk about carbon accounting because it is very similar to financial accounting, with standards, a methodology, data to collect and then to communicate. Like financial accounting with the General Accounting Plan, Sami is the origin of the General Carbon Plan, now managed by the association for the low-carbon transition (ABC), an operational guide for the implementation of carbon accounting frameworks which is today a reference.

And as in financial accounting, we can distinguish general carbon accounting from analytical carbon accounting.

2. What is general carbon accounting?

General carbon accounting provides a general view of the carbon dependence of the entity analyzed (company or community for example).

It thus seeks to measure the GHG emissions of an entity in order to then be able to reduce them and to respond to the major problem of global warming. This is what is commonly called a GHG balance sheet.

To this end, several carbon accounting tools or methodologies have been developed at national or international level. Here are the most widespread ones: the Bilan Carbone® (developed initially by the French government and the Ademe, launched in 2004, now carried by the ABC), the BEGES regulatory and at the international level the GHG Protocol and the ISO 14069 standard.

A GHG balance sheet makes it possible to record each incoming and outgoing flow of carbon and then to classify them by scopes (scopes 1, 2 and 3), by categories and by emission posts according to the nomenclature. For example, there are 6 categories and 22 emission posts in the current French regulatory methodology and 23 emission posts in the Bilan Carbone® methodology.

General carbon accounting, through the GHG balance sheet, thus fulfills several objectives, with two distinct aims.

- External aim

A GHG balance sheet can be a regulatory reporting tool. It makes it possible to communicate the greenhouse gas emissions generated by the activities of the company and by its value chain and can thus respond to increasingly ambitious French and European regulations.

In France, a BEGES (Greenhouse Gas Emission Balance Sheet) is mandatory every 4 years for companies with more than 500 employees and every 3 years for communities with more than 50,000 inhabitants and legal entities of public law employing more than 250 people (hospitals, public establishments…).

This regulatory obligation will soon extend to new companies. The new European directive on extra-financial reporting, the CSRD, thus provides for reporting on greenhouse gas emissions for companies with more than 250 employees.

Important: It is not mandatory to carry out a Bilan Carbone® to meet these regulatory obligations, even if this method allows it perfectly.

Moreover, beyond the regulatory issues, general carbon accounting also allows reporting to stakeholders. More and more companies are thus asking their suppliers to provide their GHG balance sheet or integrating the carbon footprint criterion in their calls for tenders.

- Internal aim

The GHG balance sheet as a reporting tool is not only useful externally, it is also useful internally.

Why? Because it allows to have a global vision of the greenhouse gas emissions of the company and of its value chain. In reality, the GHG balance sheet shows the company its degree of dependence on carbon. And in a world where the carbon constraint is and will become increasingly strong, this information is essential.

Thanks to general carbon accounting, the company has tools to analyze the financial risks related to the low-carbon transition to which it is exposed.

And then, general carbon accounting is the starting point of any climate strategy of a company. A GHG balance sheet indeed makes it possible to identify the main emission posts of the company and to build a reduction action plan. An Initial Bilan Carbone® perfectly allows to set up an effective transition plan, because the interest of this approach is not to fill in emission posts, but to analyze them with finesse in order to take action.

However, for certain organizations with very in-depth analysis needs, analytical carbon accounting can provide an additional level of detail.

3. Analytical carbon accounting

Whereas general carbon accounting provides an overall view of carbon dependency, analytical carbon accounting, as defined in the Analytical Carbon Accounting method provided by the ABC, allows for a detailed view of each emission item, by products, by suppliers, by site, or even by subsidiary.

Let's clarify right away that analytical carbon accounting is a subset of general carbon accounting. In other words, there is only an analytical approach if there has been a general approach beforehand. We start with the overall GHG balance to then go into detail.

This analytical approach allows for a very detailed level for organizations with specific needs for fine analysis. The goal here is to be able to detail internally the sources of emissions: item by item, site by site, subsidiary by subsidiary, etc.

The challenge is to have a very detailed understanding of the source of emissions and thus be able to build behind it an extremely targeted action plan.

Important: Analytical carbon accounting does not exclude the possibility of producing regulatory reporting. It can also be used for external reporting purposes while offering the desired level of detail internally.

The level of detail can be very detailed. But to do this, you need to categorize the company's activities and therefore the data collected during the GHG balance sheet according to the Analytical Carbon Accounting method. How to define this categorization? Two elements are important:

- The company's structure: does it have multiple sites? Several subsidiaries? Several countries where it is present? The goal is to organize your carbon accounting according to this structure.

- The company's governance: is there a manager for each site? For each subsidiary? Who drives the climate strategy? These elements also allow structuring upstream the categorization of emissions.

Analytical carbon accounting and its nomenclature are specific to each company according to the method defined by the ABC. This depends on its structure, its governance but also its sector of activity. Some examples:

- In the tertiary sector: the GHG balances of these companies often reveal a predominance of emissions from the purchase of services, the travel of employees, the construction and operation of premises. The categorization should therefore be prioritized on these emissions.

- In the textile sector: the majority of emissions from a company in this sector come from raw materials and the manufacture of products. The categorization should therefore be fine on the origin of raw materials, on suppliers, manufacturing processes.

- In the industrial sector: emissions from scope 1 and 2 are more important than in other sectors. It will be useful to push the analysis on energy consumption, by factories or by products according to suppliers or raw materials.

4. Practical example

Let's take the example of a company for which we carried out its 2022 GHG balance.

| Carbon accounting | Regulatory reporting | Distribution of emissions by scopes | Distribution of emissions by subsidiary, by suppliers, by site, etc. | Targeted action plan |

|---|---|---|---|---|

| General carbon accounting | ✅ | ✅ | ❌ | ❌ |

| Analytical carbon accounting | ❌ | ✅ | ✅ | ✅ |

Let's take the example (anonymized) of a company for which we carried out its 2022 carbon balance.

General carbon accounting

This approach allows companies to perfectly meet regulatory requirements through this complete and precise reporting of emissions, while constituting a solid basis for developing a reduction action plan.

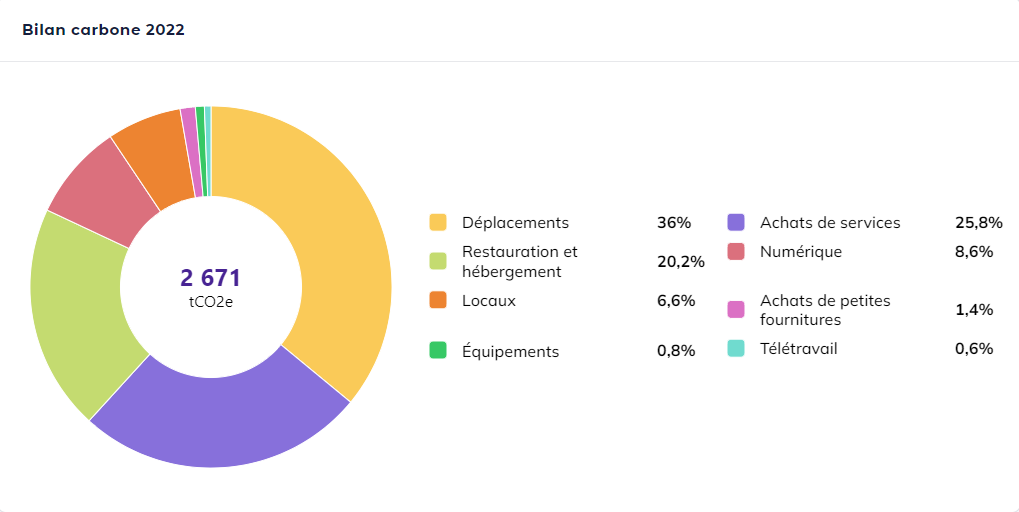

Here is a summary of its emissions.

And the summary of emissions, department by department.

Analytical carbon accounting

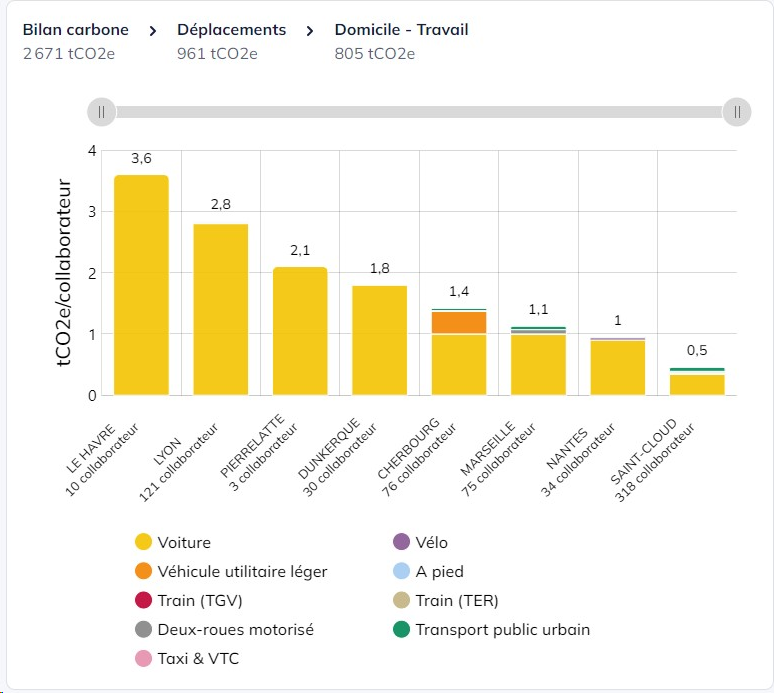

Now let's delve into a more in-depth analysis of emissions according to the analytical carbon accounting method. This approach allows for a view per employee and by company sites, offering a very high level of granularity to precisely target reduction actions.

This chart allows us to analyze the carbon intensity per employee and per site and gives us some interesting first information. Carbon intensity is thus nearly 3 times higher on the sites of Le Havre and Pierrelatte than in St-Cloud, more than 2.5 times higher in Lyon than in St-Cloud. To reduce emissions quickly and effectively, the action plan will therefore focus in priority on these sites. Moreover, another interesting element: although travel represents the most important emission item on all sites except that of St-Cloud, the premises also appear as an important source on the sites of Pierrelatte and Dunkerque. This allows the company to target measures aimed at reducing emissions from premises in priority on these two sites.

And it is possible to go even further into the details. For example, on travel, the first graph of the global distribution of emissions tells us that this is the first item of emissions at the company level with 36% of total emissions. This is a first piece of information but the analytical approach will allow us to go further.

Thus, we can first determine the employee intensity on this emission item and by company site.

The carbon intensity per employee for travel is thus very high on the sites of Le Havre and Lyon. And to a lesser extent on those of Cherbourg, Pierrelatte and Dunkerque. This will justify targeted actions on the mobility of employees on these specific sites. And we can still zoom in on this travel item.

Another example of zooming in on a particular emission item: premises. In the first graph, emissions related to premises were significant in Pierrelatte and Dunkerque. By going into detail, we realize that this is related to the recent construction of a building in Dunkerque but that it is the operation of the site that is problematic in Pierrelatte.

This granularity on emissions per site and per employee can be found in other companies by subsidiary, by entity, by product, by supplier, etc., according to the specific needs of the organization.

5. Sami, pioneer of analytical accounting

Since the launch of our platform in 2020, we have focused on a vision of the GHG inventory as an essential tool for the company's climate strategy. And that's why we have developed software that allows an analytical approach in line with the principles of the analytical carbon accounting method.

Because to have this analytical accounting, you first need to be able to associate the right data with the right emission categories and the desired level of detail. Our software allows the company to create its own nomenclature thanks to:

- More than 300 possible emission categories in order to customize and better categorize emissions

- The creation of "dimensions" and "tags" in order to precisely associate emissions with the distribution structure chosen by the company

- The creation of customized analysis indicators

The analytical approach therefore makes it possible to guide and target your action plan while being a tool for monitoring and reporting on the climate strategy.

{{newsletter-blog-3}}

Conclusion

This is not about opposing general carbon accounting and analytical carbon accounting. It's not one or the other, it's both depending on the needs. Because they are complementary.

General carbon accounting allows you to comply with regulations, have an overall view of your emissions, compare yourself with other companies in the same sector, and above all to build an effective reduction plan. An Initial Carbon Footprint® perfectly allows you to take action and define an ambitious reduction strategy.

For certain organizations with very in-depth analysis needs, analytical carbon accounting, applied according to the method defined by ABC, becomes a precious complement. Because it is this that will allow these companies to understand with very fine granularity the structure of their emissions and thus make it possible to build an even more targeted and detailed reduction plan.

Mission Décarbonation

Don't miss the latest climate news and stay ahead of regulatory changes

Your carbon footprint with Sami

Our software at the service of the analysis of your emissions and your strategy

.avif)

.avif)

Les commentaires