The "learning phase" is officially over. As we enter 2026, the Carbon Border Adjustment Mechanism (CBAM) has evolved from a mere administrative reporting exercise into a central pillar of corporate financial and strategic planning.

For the Netherlands - home to the Port of Rotterdam and serving as Europe’s primary logistics hub - the scale of this transition is more significant than anywhere else in the Union.

For Dutch importers of steel, aluminum, cement, and other carbon-intensive goods, the shift to the "definitive regime" represents a new major step.

It is no longer enough to submit quarterly spreadsheets; companies must now operate as Authorized CBAM Declarants, purchase carbon certificates aligned with EU ETS pricing, and provide audited, real-world emissions data from their global suppliers.

In a market where the Nederlandse Emissieautoriteit (NEa) and Dutch Customs are increasing their oversight, compliance has moved beyond a simple regulatory requirement to become a fundamental component of the supply chain.

This article explores the critical shifts occurring this year and provides a roadmap for Dutch businesses to manage financial risks while strengthening their position in a decarbonizing global economy.

1. What is the Carbon Border Adjustment Mechanism (CBAM)?

CBAM is an instrument established by the European Union to implement its Green Deal and combat climate change.

Adopted by the European Parliament on May 10, 2023 (Regulation (EU) 2023/956), CBAM entered its definitive phase on January 1, 2026, following a transitional phase launched in October 2023.

In practice, through the implementation of this mechanism, importers of goods (or their indirect customs representatives) must declare the direct and indirect Greenhouse Gas (GHG) emissions embedded in their imports and pay a "carbon price" on these imports when crossing the EU border.

2. What are the objectives of CBAM?

CBAM can only be understood in relation to the EU Emissions Trading System (EU ETS).

In 2005, the European Union established the EU ETS, a European carbon market that introduced a tax on CO2 emissions for producers in heavy and carbon-intensive industries. The goal was to encourage them to decarbonize their industrial processes by making low-carbon methods more competitive.

However, to mitigate the additional costs for European companies, the EU initially granted industrials numerous free allocations (free quotas). This helped limit the price per ton of CO2.

But these "free rights to pollute" are gradually disappearing, with their quantity decreasing year by year until their total elimination in 2034.

Consequently, the cost per ton of CO2 is expected to rise for European industrials, who find themselves in competition with foreign players not subject to this mechanism. This could lead to an increase in imports of products with a much higher carbon impact than those produced in the EU—a phenomenon known as "carbon leakage." This would weaken European companies while increasing global emissions, defeating the mechanism's purpose.

CBAM was designed to combat this: by taxing imports, it equalizes the carbon price paid by European industrials under the EU ETS with that of imported goods. CBAM will ramp up as free allocations disappear, and the tax level will be calculated based on the weekly average price of EU ETS emission allowances.

3. Which Dutch companies are affected by CBAM?

Several cumulative conditions determine if a company is subject to CBAM: the type of product, the nature of the trade flow, and the volume.

The company imports into the EU customs territory, the continental shelf, or the Exclusive Economic Zone (EEZ) a product listed under CBAM.

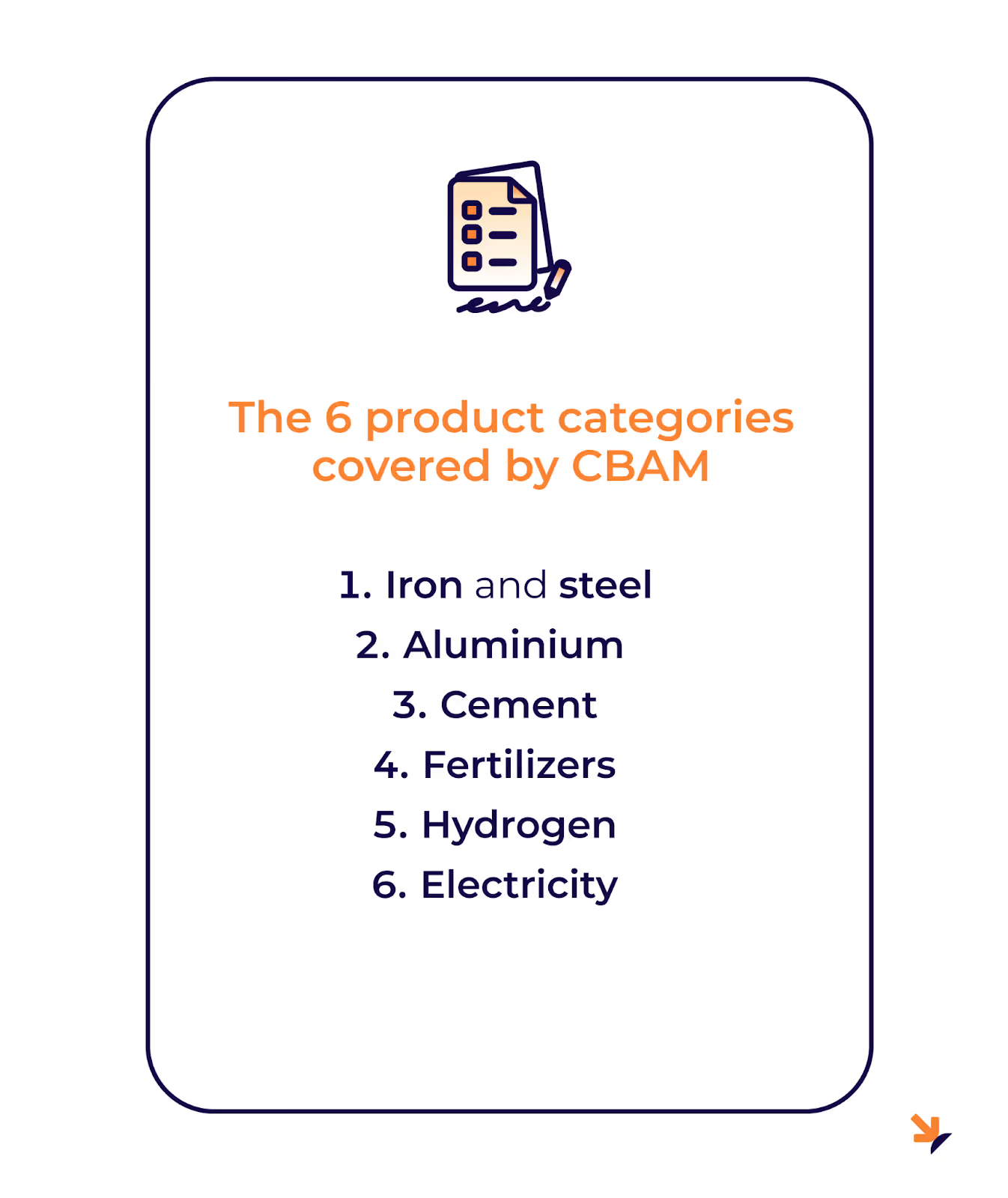

In 2026, CBAM only applies to specific product categories:

- Iron and Steel (except certain ferro-alloys)

- Aluminum

- Nitrogenous Fertilizers

- Cement

- Hydrogen

- Electricity

Note: In early 2026, several countries requested the European Commission to exclude fertilizers to avoid increasing costs for farmers. While some reports suggest the Commission may agree, this decision is not yet official.

The customs nomenclatures (CN codes) for the affected goods are listed in Annex 1 of Regulation 2023/956.

Furthermore, the imported goods must not originate from a country listed in Annex 3 (such as Iceland, Norway, Liechtenstein, or Switzerland).

Trade flows concerned by CBAM:

- It must be an "import" in the customs sense, meaning the "release for free circulation" of the goods mentioned above.

- AND the cumulative imports for a company must exceed 50 tons per calendar year. Below this threshold, importers are exempt from CBAM obligations.

This 50-ton threshold was published by the EU on October 8, 2025, as part of a simplification regulation. According to EU authorities, this measure exempts 90% of importers while still covering 99% of CO2 emissions related to CBAM products.

4. The Shift to the "Definitive Regime": What are the obligations for Dutch companies?

The transitional period, which began in October 2023, ended on December 31, 2025. During that phase, companies submitted quarterly reports.

Since January 1, 2026, the following obligations apply:

The "Authorized Declarant" Status

Obtaining the status of Authorized CBAM Declarant is mandatory to import CBAM-covered goods.

- First, you need an eHerkenning ID with at least a reliability level of EH3. If you already have eHerkenning, you must activate the CBAM service.

- You must then submit your application through the CBAM Registry portal.

- Warning: Without this status, goods will be blocked at customs.

Flexibility for early 2026: Importers who submit their application before March 31, 2026, may continue to import while their application is being processed by the Nederlandse Emissieautoriteit (NEa).

However, if the NEa ultimately rejects the application, they are obligated to issue a fine for "importing without authorization."

Submission of the Annual CBAM Declaration

Quarterly reports are replaced by an Annual Declaration. It must include:

- Total quantities imported

- Production processes used

- Direct and indirect emissions associated with the goods

- Specifics on the calculation methodology used

The first annual declaration for 2026 imports must be submitted by September 2027.

Acquisition and Surrender of CBAM Certificates

Starting in 2027, all Dutch declarants must surrender CBAM certificates each year corresponding to the emissions imported the previous year.

- 1 certificate = 1 ton of CO2.

- The European Commission will publish the certificate price weekly, based on the average EU ETS auction prices. The certificate price could settle between €80 and €100 in 2026, according to current EU ETS data.

- The purchase platform is expected to open in February 2027.

5. Financial & Supply Chain Impact for Dutch Businesses

Cost Modeling: How to estimate the "Carbon Tax" on key imports?

The calculation for purchasing certificates is as follows:

Number of CBAM Certificates = Embedded Emissions (tonnes CO₂) × EU ETS Price

Two factors can reduce the number of certificates to be purchased:

- Carbon price paid in the country of origin: If a carbon price has already been paid abroad, it is converted into CO2 tons and deducted from the certificates to be surrendered.

- EU ETS Free Allocations: A correction is applied to ensure importers are not penalized compared to EU producers still receiving free quotas. These free allocations will decrease from 2026 to 2034.

Important: From 2027 onwards, Dutch importers must ensure that at the end of each quarter, their account holds a minimum of 50% of the certificates covering the emissions imported since the beginning of the year.

Supplier Engagement

How are emissions calculated?

- Actual Values: Based on data provided by the supplier (Highly recommended).

- Default Values: Published by the European Commission.

Actual values are preferred because they are more accurate; default values are typically higher (penalizing), leading to higher costs. Using actual values requires the supplier to calculate emissions and have them certified by an accredited independent verifier.

For 2026, it is advised to use default values for cost estimation while preparing your suppliers for the 2027 certification requirements.

6. Port of Rotterdam CBAM impact

There are several possible scenarios for importers whose goods enter Europe via the Port of Rotterdam.

Scenario 1: You are the Dutch Importer

In this case, you import the goods (steel, aluminum, etc.) into Rotterdam to resell them to European customers.

- Your Responsibility: You are the Authorized CBAM Declarant. You are responsible for managing the entire process with the NEa, purchasing CBAM certificates, and submitting the annual declaration.

- Commercial Impact: You must integrate the cost of CBAM certificates into your final selling price. Your European customers have no direct reporting obligations, but they depend on your compliance to secure their own supply chain.

- Risk: If your emissions data is incorrect, your company is exposed to fines from the NEa, not your customers.

Scenario 2: You Act as an Indirect Customs Representative

You are a Dutch freight forwarder or logistics company clearing goods for a foreign client not established in the Netherlands.

The Strategic Choice:

- Acceptance: You agree to be the Authorized CBAM Declarant for your client. You then bear the legal and financial responsibility for the certificates. While this is a high-value service, it carries a financial risk regarding the client’s solvency to reimburse the certificates.

- Refusal: You decline to take on CBAM responsibility. Your foreign client must then obtain their own authorized declarant status from their national authority. In this case, you only handle standard customs clearance.

Important: Even as an Indirect Customs Representative, you are not automatically responsible for CBAM. This is a contractual decision between you and your client. CBAM responsibility can be decoupled from standard customs representation, but this must be clearly established in your service agreements.

Scenario 3: Logistics Hub under Customs Transit

The goods arrive in Rotterdam but are placed under a transit procedure. They leave your warehouse or terminal to be cleared through customs later, for example, in Paris.

- Your Role: As a Dutch company, you are merely a logistics link or a technical point of entry.

- CBAM Responsibility: You have zero responsibility. The CBAM obligation is only triggered at the time of "release for free circulation" (final customs clearance).

- Action: The final consignee in France must ensure they are an Authorized CBAM Declarant with the French authorities. You do not need to purchase certificates or report to the NEa for these transit flows.

7. Compliance Checklist: 5 Steps for 2026

- Step 1: Confirm your status with the NEa and ensure your eHerkenning EH3 is active.

- Step 2: Audit your current supplier data and identify "high-risk" (high-carbon) suppliers.

- Step 3: Establish a "Carbon Cash Flow" forecast to anticipate certificate costs in 2027.

- Step 4: Secure a third-party verifier early (scarcity of auditors is a major risk).

- Step 5: Update purchase contracts to include "Carbon Reporting Clauses."

8. Key deadlines for 2026-2027

- March 31, 2026: Importers have to submit their application before March 21, 2026 to continue to import while their application is being processed by the Nederlandse Emissieautoriteit (NEa).

- February 2027: Opening of the purchase CBAM certificates platform

- September 2027: First annual declaration for 2026 imports

- 2027 : Dutch importers must ensure that at the end of each quarter, their account holds a minimum of 50% of the certificates covering the emissions imported since the beginning of the year

FAQ

Q1: What happens if my CBAM declarant status is pending in 2026?

If you applied before March 31, 2026, you can import while the NEa processes your file. However, ensure your data is compliant, as a rejection will lead to significant fines for unauthorized imports.

Q2: What is the minimum threshold for CBAM reporting in the Netherlands?

The threshold is 50 tonnes of CBAM goods per year. If your cumulative imports are below this weight, you are exempt. Note that this threshold does not apply to Hydrogen or Electricity.

Q3: How much will a CBAM certificate cost?

The price is not fixed; it fluctuates weekly. It mirrors the average price of the EU ETS. In 2026, prices are expected to hover between €80 and €100 per tonne of CO2, but you should monitor the weekly EU Commission publications.

Q4 : Can CBAM certificates be refunded?

Yes. If a declarant has purchased more certificates than actually required, they may request a buy-back by the Commission, up to a maximum of one-third of the certificates purchased during year N-1. The request must be submitted by November 30th of the year of surrender. The buy-back price shall be equal to the price paid at the time of purchase.

Q5: Do I need a specific ID to access the CBAM Registry?

Yes. In the Netherlands, you must use eHerkenning with a minimum reliability level of EH3. You must also ensure that the "CBAM" service is specifically activated on your account by your provider.

Q6: What happens if my supplier refuses to provide emissions data?

If your supplier does not provide actual data, you must use the EU Default Values. These are designed to be higher than average, meaning you will likely pay more for your CBAM certificates than if you had actual data.

Mission Décarbonation

Don't miss the latest climate news and stay ahead of regulatory changes

Les commentaires